Authors: Conor Gunn, EY Ireland Government and Infrastructure Partner and Nabeel Raza, EY Ireland Government and Infrastructure Advisory Associate Director

Upcoming legislative changes around sustainability and evolving market trends are expected to have a major impact on the real estate sector.

In brief

- Real estate owners and occupiers need to act now to minimize the impact on their real estate assets, including the risk of a ‘brown discount’ and the potential for assets to become ‘stranded’.

- While different options are available, it is crucial to have a robust real estate strategy in place from an early stage. This is particularly important for a portfolio of assets since options like retrofitting or potential sale and relocation demand careful planning and time for effective implementation.

Currently, the construction and real estate sectors contribute around 39% of all global CO2 emissions. However, significant changes are underway that are likely to rectify the present state and move the sector towards a more sustainable future. These changes include shifts in market trends, as sustainability credentials become increasingly important for occupiers, investors, and landlords driven by stakeholder expectations and the need to act responsibly, given the ambitious ESG targets set by companies. More recently however, the changing legislative context has also emerged as a significant driver for the reduction of carbon emissions in the real estate industry.

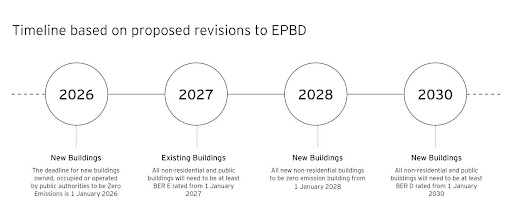

The Energy Performance of Buildings Directive 2010/31/EU (amended in 2018 by Directive 2018/844/EU) (EPBD) is critical European-level legislation that mandates improvements in the energy efficiency of buildings. The revisions to the EPBD form part of the EU’s Fit for 55 Package, which aims to facilitate the reduction of greenhouse gas emissions by at least 55% by 2030. According to the revised directive following deadlines for new and existing non-residential buildings have been proposed:

The directive will undergo negotiations involving the European Parliament, European Council, and European Commission before it can be enacted. EU member states, including Ireland, will need to adopt different measures to achieve these targets through national renovation plans. Hence, now is an appropriate time for landlords and occupiers to start preparing and positioning their CRE portfolio for transition before the legislation comes into effect. At that point, there will be limited time to plan, prepare, and execute a strategy to transition the CRE portfolio to meet the upcoming requirements.

Impact on the CRE sector in Ireland

We are already witnessing the impact of market expectations and legislative changes on the commercial real estate (CRE) sector, with rising demand for sustainable buildings. One key component of the CRE industry is the ‘Office Market’ comprising office buildings, owned, or occupied by private sector and public sector employers. The effect of these changes is likely to be felt more strongly in the Office Market due to the large number of employees and companies associated with it.

The demand for ‘New, Clean & Green’ office space is rising in the Irish market. Buildings with BER A3 and LEED Gold or BREEAM Excellent certifications are highly sought after. Although currently in relative undersupply, the stock of sustainable properties is expected to increase in response to growing trends and legislative requirements.

Given the current mismatch, CRE assets with industry leading sustainable ratings often have a ‘Green Premium’ over typical properties. As buildings with strong environmental performance tend to be newer, premium assets, it can be challenging to determine the sustainability premium. Nevertheless, there market research suggests that green buildings command higher rents over comparable non-green properties with a Green Premium in rents across some European cities averaging 21%¹ over a 5-year period.

On the other hand, properties with lower sustainability ratings are expected to experience a ‘Brown Discount’ which, according to market research, can range between 10%-30%. The changing legislative context is expected to result in more properties experiencing this discount if they are unable to upgrade on a timely basis.

In the worst-case scenario, legislative changes like the proposed revisions to EPBD may even result in older and less efficient properties becoming ‘Stranded Assets.’

In Ireland, there are approximately 210,000² commercial buildings. Based on the results of approximately 70,000 BER audits carried out on non-domestic buildings between 2009 and 2022 almost 19%³ of the non-domestic were rated BER F or BER G, indicating a significant number of non-domestic buildings are likely to require an upgrade in coming years.

The upcoming legislation is also likely to increase the risk of unsustainable assets becoming stranded (for example buildings rated BER F and G at present) if the energy performance cannot be improved or is not viable. This is likely to have a major impact on older stock as has been the case in England and Wales, where from April 2023 buildings not meeting minimum EPC rating requirement of E or above cannot be leased or sold, likely leading to vacancies in properties not meeting this standard, unless an exemption is received. To avoid this happening, the landlords and investors will proactively need to manage the at-risk assets and consider the development of a CRE strategy to transition the existing CRE portfolio towards a more sustainable state to avoid a significant write-down in values.

What can investors and occupiers do?

The amount of work needed to transition a real estate portfolio to a sustainable one can be substantial and is often underestimated. Therefore, for those aiming to align their real estate portfolio with net-zero goals or comply with emission reduction regulation, time becomes a critical factor.